Unadjusted Trial BalanceHow to Prepare one with Examples

It’s the end of an accounting period which means it is time to prepare your financial statements.

Before we can proceed with the actual preparation of financial statements, there is a step we have to go through first – the preparation of the trial balances.

You will need to prepare three trial balances: the unadjusted trial balance, the adjusted trial balance, and the post-closing trial balance.

Of the three, you will have to prepare the unadjusted trial balance first, followed by the adjusted trial balance.

You’ll be preparing the unadjusted and adjusted trial balance once a month if your business is reporting financial statements on a monthly basis.

As for the post-closing trial balance, it is typically only prepared at the end of the reporting period (usually after a full year period).

This article will provide you with information about the first of the three trial balances: unadjusted trial balance.

You will learn what an unadjusted trial balance is, why is it prepared, and how it is prepared.

Even if you’re not the one in charge of the preparation of financial statements, this article will still be a worthwhile read.

Having a little bit of accounting knowledge will help you get a better understanding of your business’s financial conditions.

What is an unadjusted trial balance?

An unadjusted trial balance is a listing of all the accounts found in a general ledger.

It is prepared at the end of the period (e.g. month, quarter, year) before any adjusting entries are made.

It is usually used as a starting point for analyzing account balances.

As its name implies, the account balances must be balanced, meaning that total debit and credit balances are equal.

As an unadjusted trial balance is prepared before any adjusting entries are made, it’s not a suitable reference for preparing financial statements.

Rather, think of it as an organized listing of the accounts found in the general ledger.

Accounts are listed in a way that you’d present your balance sheet and income statement: assets first followed by liability and equity, then revenue items followed by expense items.

An unadjusted trial balance’s purpose is to make sure that the balances are arithmetically correct.

If there are any errors, they should be detected and corrected.

An error can be as simple as entering a debit balance as a credit balance(and vice versa), or it could be as complicated as failing to post a journal entry.

Typically, these corrections are not yet considered as the adjusting entries that you’ll see once the preparation of an adjusted trial balance is started.

Since no adjusting entries are made yet, expect that most of the figures presented in an unadjusted trial balance are not the ones you’ll see in financial statements.

An unadjusted trial balance is suitable for accounting systems that use the double-entry system.

Why prepare an unadjusted trial balance?

The preparation of financial statements has to start somewhere.

While it is possible to use your general ledger as a reference for the preparation of financial statements, it is inefficient.

That’s why you must prepare a trial balance (adjusted trial balance or post-closing trial balance) that can be used as a reference.

The unadjusted trial balance is just the first of the three trial balances that you’ll have to prepare.

If we compare it to the publishing of a book, the preparation of the trial balances is the editing phase.

The unadjusted trial balance is our very first draft.

The adjusted and post-closing trial balances are our edited draft.

The financial statements are our final product.

It should be noted though that in some automated accounting systems, the preparation of trial balances is no longer needed.

Specifically accounting systems wherein unbalanced GL posting are not allowed, which serve the purpose of ensuring that debit and credit balances are equal.

That said, not every business uses an automated accounting system.

The practice of preparing trial balances still exists today because of this.

With that, let me present to you some of the purposes of an unadjusted trial balance:

Organizes accounts for the preparation of financial statements

A trial balance, such as the unadjusted trial balance, is typically formatted in a way similar to what you see in a balance sheet or income statement.

That is- Assets first, Liabilities and Equity next, then followed by Revenue items and Expense items.

As for assets, they are ordered according to liquidity where the most liquid asset, cash, is listed first.

For liabilities, current liabilities are listed first, then next are non-current liabilities.

For expenses, the cost of sales is listed first then next are operating and non-operating expenses.

Alternatively, the accounts can be listed sequentially according to their account number in the chart of accounts.

Summarizes Balances

A general ledger typically shows us the balance of each account.

However, it does not present us with the total debit and credit balances.

For that, we refer to the trial balances, unadjusted trial balance included.

A trial balance will typically summarize the debit and credit balances.

Checks mathematical accuracy

Since an unadjusted trial balance employs the double-entry system, it’s not enough that it provides us with the total debit and credit balances.

It must ensure that they are equal per the double-entry system.

As such, it must also ensure that the balances are mathematically accurate.

Error Detection

With an unadjusted trial balance, detecting errors is faster and easier.

If the total debit and credit balances don’t match, then that means that there is an error.

It could be as simple as a clerical error in transferring data from the general ledger to the unadjusted trial balance.

Or it could be as deep as an error in the journal entry or general ledger posting.

Either way, an error is obvious if the debit and credit balances are not equal.

For management use

Unadjusted trial balances are fast and easy to prepare compared to financial statements.

This is helpful for internal use when employees need timely data for their reports.

It gives them an idea of how much cash is available, what the level of revenue is, the status with debtors and creditors, etc., even before the actual financial statements are prepared.

Do note that trial balances are for internal use only.

As they don’t necessarily comply with the GAAP or IFRS, they are not suitable for external use.

Provides a basis for adjustments

The unadjusted trial balance is an unadulterated listing of the accounts from the general ledger.

As such, no adjustments are made to them yet.

The unadjusted trial balance is a good basis for making adjusting entries as it conveniently lists all the accounts that may need adjustments (prepaid expenses, accruals, deferred revenue, etc.) and put them in one place.

How to prepare an unadjusted trial balance

The first thing we need to do when preparing an unadjusted trial balance is to decide on the format to be used.

A simple unadjusted trial balance will look like this:

![]()

![]()

It has three columns: Account Title, Debit, and Credit.

The account title column is where the accounts from the general ledger are entered.

Meanwhile, the debit column is where debit balances are entered.

Asset and Expense accounts typically have debit balances.

Lastly, the credit column is where we enter credit balances.

Liability, Equity, and Revenue accounts typically have credit balances.

Now that we have our blank unadjusted trial balance, the next step is to fill it.

Listing the balance sheet accounts is our next step.

As per a typical balance sheet presentation, we first list the asset accounts.

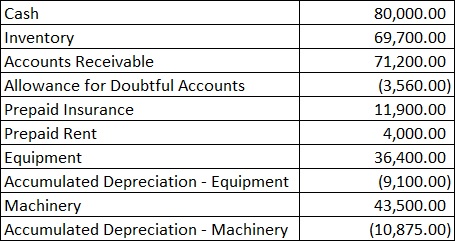

Suppose that company X has the following asset accounts:

Notice that there are negative balances.

These accounts are contra-asset accounts and typically have credit balances.

With that in mind, let’s enter these asset accounts into the unadjusted trial balance:

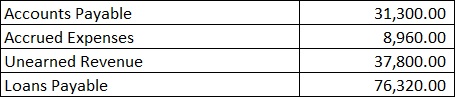

The next step is to list liability accounts.

Just like with a balance sheet, current liabilities are listed first, followed by non-current liabilities.

Suppose that company X has the following liability accounts:

Liability accounts typically have credit balances.

With that in mind, let’s post these liability accounts into company X’s unadjusted trial balance:

The last of the balance sheet accounts to be listed are the equity accounts.

Just like liability accounts, equity accounts typically have a credit balance.

Suppose that company X has the following equity accounts:

Let’s enter these account into company X’s unadjusted trial balance:

And with that, we listed all of company X’s balance sheet accounts.

To summarize, asset accounts typically have debit balances (contra-asset accounts have credit balances).

Liability accounts and Equity accounts have credit balances.

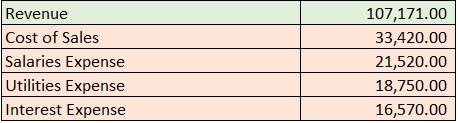

The next step is to transfer the income statement accounts to the unadjusted trial balance.

Revenue accounts, such as sales revenue and service revenue, typically have credit balances.

Expense accounts on the other hand have debit balances.

Suppose that company X has the following income statement accounts:

Accounts highlighted in green are revenue accounts, while those highlighted in red are expenses accounts.

With that in mind, let’s enter these income statement accounts into company X’s unadjusted trial balance:

And with that, both balance sheet and income statement accounts are entered into the unadjusted trial balance.

The next step is to ensure that total debit and credit balances match, meaning that they are equal.

To do that, we add all debit balances and all credit balances separately:

As per computation, both debit and credit balances match with the amount being $406,960.00.

With that, company X’s unadjusted trial balance is complete.

However, if the debit and credit balances didn’t match, there’s another step we need to take which is error detection and correction.

What to do when the unadjusted trial balance is not balanced

If the debit and credit balances don’t match, then there is an error somewhere in the accounting process.

The obvious thing to do is to look at the journal entries and ledger postings, right?

Well, there are simple corrections you can do before resorting to that.

It could be that the error was made when transferring the general ledger accounts to the unadjusted trial balance.

In such a case, you usually won’t have to review your journals and ledgers.

Try recomputing your balances

It could be that the error is just a mathematical error.

It could be that you missed including an account in the computation.

Try recomputing your total debit and credit balances and see if that works.

If not, then let’s proceed to the next step.

Divide the difference by two (2)

If the difference between the debit and credit balances is divisible by two, it could be a simple error of posting a debit balance as a credit balance (or vice versa).

In such a case, try dividing the difference by two.

Then look for an amount in the unadjusted trial balance equal to the resulting figure.

If the debit balance is greater than the credit balance, it could be a case of debiting a credit balance.

If the credit balance is greater, then it could be a case of crediting a debit balance.

For example, here is an unadjusted trial balance with such error:

As can be seen above, the debit and credit balances do not match (the credit balance is greater).

The difference between the two is $8,000.

Divide it by two, we get $4,000.

Now let’s check if there is a credit balance (since the total credit balance is greater) with the same amount:

Highlighted in green is the prepaid rent account with a credit balance of $4,000.

Prepaid rent is an asset account and should have a debit balance.

To correct this error, we simply move the balance from the credit column to the debit column:

Check if the difference is divisible by nine (9)

If the “divide by two” trick does not work, then the error may be a transposition or slide error.

A transposition error occurs when two digits are interchanged in an account balance.

For example, entering $6,900 as $9,600 or entering $15,600 as $16,500.

A slide error occurs when a decimal point is incorrectly placed.

For example, entering $200 as $2,000 or entering $90,000 as $9,000.

To check if you made either error, check if the difference is divisible by 9.

If it is, then you either made a transposition or slide error.

Compare the trial balance accounts with their respective general ledger account balance to confirm that the error is indeed a transposition or slide error.

To illustrate, here is an unadjusted trial balance with a transposition error:

As per computation, the difference between the debit and credit balances is 900 which is divisible by 9.

Upon review with the general ledger, the accounts receivable balance should be $71,200 instead of $72,100.

To correct the error, just enter the correct accounts receivable balance which is $71,200:

Other causes of error

If both the “divide by two” and “divisible by nine” tricks didn’t work, then the error may be caused by one of the following:

- An error in a journal entry (e.g. a journal entry with unequal debit and credit entries)

- Posting a journal entry to the wrong general ledger account

- Failing to include an account in the trial balance

- The error originated in the general ledger (e.g. wrong computation of totals)

In such cases, there is no other choice but to review your journals and ledgers until you find the cause of the error.

If an unadjusted trial balance is “balanced”, does that mean that it is error-free?

Not quite.

Even if an unadjusted trial balance is “balanced”, there could still be errors that don’t result in mathematical inconsistencies.

These errors may be caused by the following factors:

- Omitting a journal entry or ledger account

- Error in principle – a transaction is incorrectly recorded in the journals. For example, recording a purchase of supplies as a purchase of inventory

- Error of original entry – the journal entry itself is incorrect. The debit and credit entries could be either overstated or understated.

- Reversal of debit and credit entries – it could be that amounts recorded are correct, however, the debit and credit entries were reversed. For example, for payment of purchases, it could be that “cash” is debited instead of credited, and “purchases” is credited instead of debited

- Duplication of journal entries or ledger accounts

It’s impossible to detect such errors just by looking at the unadjusted trial balance.

In such cases, a review of the journals and ledgers is required.

FundsNet requires Contributors, Writers and Authors to use Primary Sources to source and cite their work. These Sources include White Papers, Government Information & Data, Original Reporting and Interviews from Industry Experts. Reputable Publishers are also sourced and cited where appropriate. Learn more about the standards we follow in producing Accurate, Unbiased and Researched Content in our editorial policy.

Open Learn "2.6 Balancing off accounts and preparing a trial balance" Page 1 . December 3, 2021

Ohio University "What Is a Trial Balance?" Page 1. December 3, 2021