Net Income Formula

Net income is a business’s earnings after considering all expenses.

It considers all income and expenses from all sources (operating activities, investing activities, and financing activities).

Net income not only shows the efficiency of a business’s operations, but it also shows how well a business is managing its investing and financing activities.

It captures the effect of one of the most common non-operating expenses: the cost of borrowing.

Net income is one of the most important figures in a business’s financial statements.

It basically summarizes the financial performance of a business in a given period.

It also includes the items that the gross profit and operating income don’t capture.

That is why it’s important to know how to compute your business’s net income.

The Net Income Formula

Computing for net income is actually fairly simple.

You only need to add up all income generated by your business, and then deduct all expenses incurred.

Put into formula form, it should look like:

Net Income = Income from all sources – Expenses from all sources

Simple right?

But it’s still a little vague, so let’s try breaking it down even further.

“Income from all sources” means a business’s earnings from all income-generating activities.

This includes the revenue you earn from your business’s operations and the income you receive from non-operating activities such as the gain from the sale of a long-term asset, the interest income from the money lent to another business, or the dividend received from the shares of another business.

So if we expound on this component of the formula, it would look like:

Income from all sources = Revenue + Non-operating Income

“Expenses from all sources” means all the expenses incurred by a business.

This includes the cost of the goods sold or services that are offered by a business, the operating expenses incurred such as rent, salaries and wages, utilities expense, etc., and the non-operating expenses such as the cost of borrowings (e.g. interest expense, financing costs), the losses due to fire, the loss from the sale of a long-term asset, etc., and the income tax required to be paid by the government.

Similar to what we did with “income from all sources”, we expound on this component and we get:

Expenses from all sources = Cost of Sales + Operating Expenses +

Non-operating Expenses + Income Tax

Put together, we get the formula:

Net Income = (Revenue + Non-operating Income) – (Cost of Sales + Operating Expenses + Non-operating Expenses + Income Tax)

That made things clearer right?

What’s more, these are the line items that you can usually find in a business’s income statement.

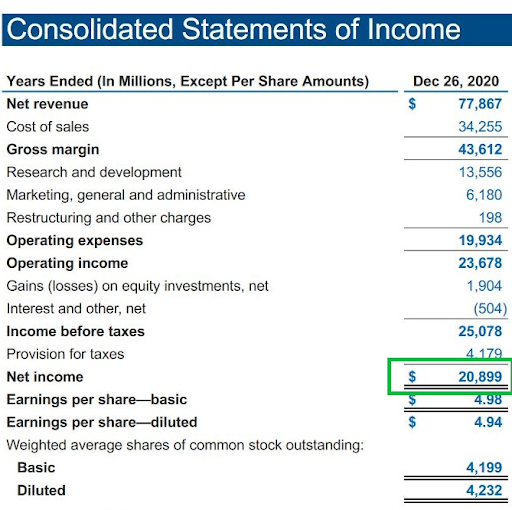

Let’s try using it on the following income statement and compute the net income:

Here we have a net revenue of $77,867,000,000, cost of sales of $34,255,000,000, operating expenses of $19,934,000,000, non-operating income of $1,904,000,000 in the form of net gains on equity investemts, non-operating expenses of $504,000,000 (interest and others), and provision for taxes (income taxes) of $4,179,000,000.

Let’s compute for net income using our formula:

Net Income = (Revenue + Non-operating Income) – (Cost of Sales + Operating Expenses + Non-operating Expenses + Income Tax)

Net Income = ($77,867,000,000 + $1,904,000,000) – ($34,255,000,000 + $19,934,000,000+ $504,000,000 + $4,179,000,000)

Net Income = $79,771,000,000 – $58,872,000,000

Net Income = $20,899,000,000

And so we arrive at a net income of $20,899,000,000.

If we were to compute for it using Microsoft Excel, it should look like:

And we still arrive at a net income of $20,899,000,000

Let’s check if we got it right:

And it seems like we got it right.

This is actually an excerpt of Intel Corporation’s income statement which can be accessed here (page 76).

Net Income and Financial Ratios

Since net income is a quantitative representation of a business’s overall financial performance, it can also be used for certain financial ratios.

It can be used for the following financial ratios:

Net Profit Margin

The net profit margin (also known as profit margin or net margin) is a financial ratio that measures how much net income a business is earning from its revenue.

It is often presented as a percentage and represents how much net income a business actually earns from its sales of goods or services.

It can be computed using the following formula:

Net profit margin is calculated by dividing a company’s net income by its total revenue: Net Profit Margin = Net Income ÷ Revenue.

For example, if a business has a revenue of $100,000 and a net income of $20,000, then it has a net profit margin of 20%.

It can also be interpreted that the business is earning $0.20 of net income per $1.00 revenue.

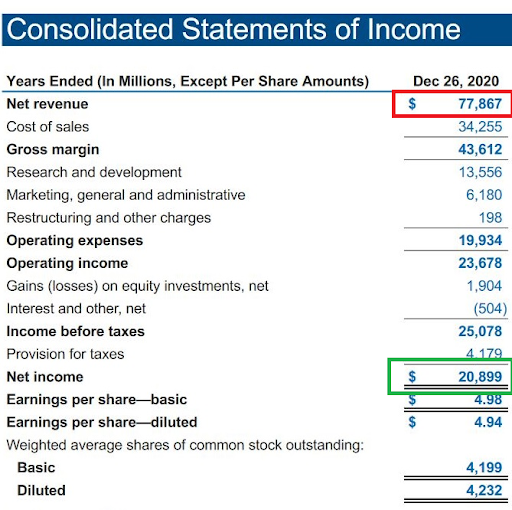

Let’s try using it with Intel Corporation’s income statement:

The one highlighted with the red box is the revenue figure, while the one highlighted with the green box is the net income figure

Net Profit Margin = Net Income ÷ Revenue

Net Profit Margin = $20,899,000,000 ÷ $77,867,000,000

Net Profit Margin = 0.27 or 27%

As per our computation, Intel Corporation’s Net Profit Margin for the year ended December 2020 is 0.27 or 27%.

This meant that for every $1.00 of revenue it earned, it had a $0.27 net income.

It is important to be mindful of your business’s profit margin.

Monitor it along with your other financial ratios, such as the operating margin.

Keep track of its changes monthly, quarterly, or annually and assess whether the business is operating within its expected level, or if forecasts and budgets should be modified.

Compare it with your business’s operating margin to assess if there’s a significant difference between the two, and to see if some changes should be made with the business’s investing and financing policies.

For example, if the operating margin is 40%, and the net profit margin is 13%, then there is a 27% difference between the two, and it is found out that a majority of this difference is caused by interest expense.

The business can then decide to slow down with its borrowings until its level of operating income can keep up with its level of borrowings.

The net profit margin is also better than the net income when it comes to comparing with other businesses or with the industry standard.

Since it’s expressed as a decimal or percentage, it doesn’t matter if there’s a huge difference between the sizes of businesses being compared so long as they are within the same industry.

Return on Assets

Return on Assets (ROA) is a financial ratio that measures the efficiency and profitability of a business.

It measures how much net income a business is earning from its assets.

Or it can also be interpreted as how much profit is being returned to a business’s investment in assets.

It can be computed by using the formula:

Return on Assets = Net Income ÷ Average Total Assets

-or-

Return on Assets = Net Income ÷ Ending Balance of Total Assets

The higher the ROA is, the better it is for the business.

It means that the business is doing great in generating the most profits and getting the most bang-for-buck from its assets.

For example, we have two friends Ivan and Iona who both decided to start a food cart business.

Ivan laid out $30,000 for the most basic food cart, enough to cook and serve food.

Iona on the other hand spent $100,000 for a unicorn-themed food cart, with a menu that is unicorn-themed as well.

After a month, Ivan had earned $4,500 after considering expenses, while Iona earned $12,000.

Assuming that they both don’t have any other assets invested in their respective businesses, let’s compute for their respective ROAs.

If we just base it on the quantitative value of their net income, we can say that Iona is the winner between the two with her net income of $12,000 compared to Ivan’s $4,500.

But if we take a look at their ROAs, Ivan actually had it better with a ROA of 15% compared to Iona’s 12%.

This means that while Iona had a greater net income dollar-wise, Ivan had the better bang-for-buck out of his food cart business.

Return on Equity

Return on Equity (ROE) is another financial ratio that measures the efficiency and profitability of a business.

While the ROA did not consider the debt aspect of a business, the ROE does.

It measures how profit is returned to the investments by the business’s owners and/or investors.

If the business is 100% equity financed, then ROE will be equal to ROA.

The ROE of a business can be computed using the formula:

Return on Equity = Net Income ÷ Average Shareholder’s Equity

-or-

Return on Equity = Net Income ÷ Ending Balance of Shareholder’s Equity

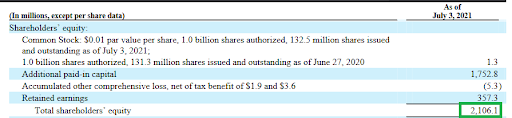

Let’ try using the formula to compute Performance Food Group Company’s return on equity.

Below are excerpts of Performance Food Group Company’s financial statement for the fiscal year ended July 3, 2021, the first being its financial statement with the net income highlighted, and the second being the shareholders’ equity portion of its balance sheet with the shareholders’ equity highlighted:

We will be using the second variation of the ROE formula for this example:

Return on Equity = Net Income ÷ Ending Balance of Shareholder’s Equity

Return on Equity = $40,700,000 ÷ $2,106,100,000

Return on Equity = 0.02 or 2%

As per computation, Performance Food Group Company’s ROE is 0.02 or 2%.

This means that for the fiscal year ended July 3, 2021, it earned $0.02 net income for every $1.00 of equity.

Having good ROE would mean that the business doing great in making the most profit out of the investments made by its owners and/or investors.

It could also entice potential investors as having a high ROE would mean that if they invest in such a business, the return on their investment would be potentially high.

Earnings per Share

The earnings per share (EPS) is a financial ratio that measures the amount of net income earned by each share of a business’s outstanding stock.

This ratio only applies to corporations and other business entities that issue stocks.

It is useful in that it is a potential driver that can influence the market value of a share.

Earnings per share can be computed by using the formula:

| Earnings Per Share = | Net Income/ |

| Number of Outstanding Shares |

Or if a company has preferred shares, the following formula should be used instead:

| Earnings Per Share = | Net Income – Dividends for Preferred Shares/ |

| Number of Outstanding Common Shares |

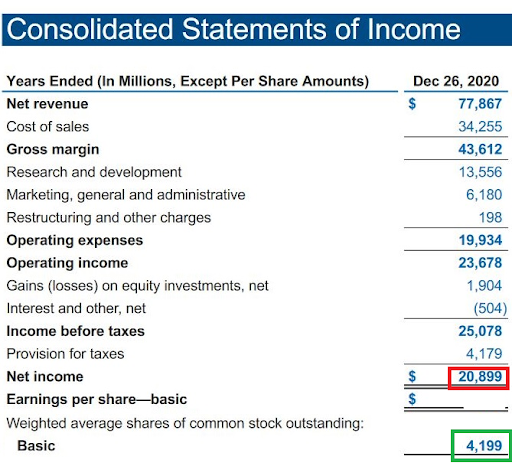

Let’s go back to Intel Corporation’s income statement and compute for its earnings per share:

The one highlighted with the red box is the net income figure, while the one highlighted with the green box is the number of outstanding shares

Earnings per share = Net Income ÷ Number of Oustanding Shares

Earning per share = $20,899,000,000 = 4,199,000,000

Earnings per share = $4.98

This means that each outstanding share of Intel Corporation earned $4.98.

This isn’t necessarily the market value of each of its shares, but it can influence their potential market value.

If Intel were to distribute all of its net income as dividends, then each share would receive $4.98.

FundsNet requires Contributors, Writers and Authors to use Primary Sources to source and cite their work. These Sources include White Papers, Government Information & Data, Original Reporting and Interviews from Industry Experts. Reputable Publishers are also sourced and cited where appropriate. Learn more about the standards we follow in producing Accurate, Unbiased and Researched Content in our editorial policy.

Intel Corporation "Form 10-K" Page 76. September 22, 2021

IRS.gov "Tax Statistics" Page 1 . September 22, 2021

Easternct.edu "Page 1 of 2 What are the 11 Basic Accounting Formulas?" Page 1. September 22, 2021